Good Credit Info’s LendingClub Review

LendingClub in a Nutshell

LendingClub is America’s most recognizable name in Peer to Peer (P2P) borrowing. American P2P has had some difficult early years, but the basic concept – people lending money to other people online, at great rates, with lots of safety measures – is stellar. LendingClub has pioneered this concept in the United States. Today, they are the national face of P2P lending/borrowing.

The LendingClub Story

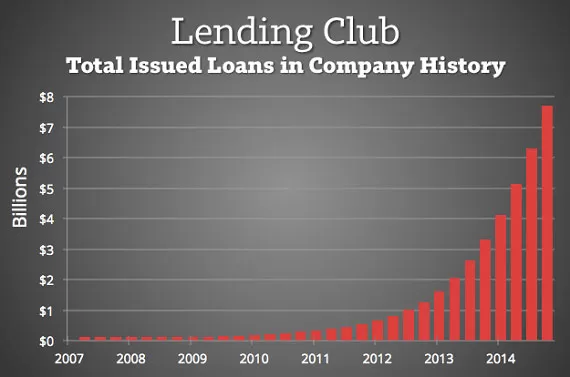

LendingClub started out as one of Facebook’s first apps, way back in 2007. LendingClub was the first company to put loan trading on a secondary market, where investors can buy and sell financed loans. This model is now used by dozens of companies, but LendingClub is still the biggest. $16 Billion in loans had been issued through LendingClub by the end of 2015. The recent resignation of CEO/Founder Renaud Laplanche has raised a lot of questions about LendingClub, but their fundamentals seem strong. At the end of the day, we still believe that LendingClub is an amazing resource for people who have been denied loans from traditional lenders.

LendingClub’s Methods

LendingClub pairs lenders with borrowers on a market they created for the LendingClub platform. Since this LendingClub review is focused more on the borrower experience, we won’t go into great detail about the lender experience. For borrowers, the process is pretty straightforward, but it’s built on some complex algorithms. First, we’ll talk about the loan process from the user’s perspective, then we’ll talk about what’s actually going on behind the scenes.

Let’s say you want to borrow money, but your loan request was denied by your local bank. You might also need money five days from now, but your bank said that the soonest your money could be accessible is two weeks from now. Common situations like these caused Peer to Peer Lending to evolve. Today’s LendingClub borrowers can receive personal loans between $1,000 and $40,000, or business loans up to $100,000. Loans are issued at APR rates between 6.95% (Awesome!) and 35.89% (Yikes!). We’ll talk more about this huge range in prices later.

New borrowers complete a brief loan application. LendingClub does a soft credit check (doesn’t lower your credit score) with the three Credit Reporting Agencies to determine if the applicant qualifies. LendingClub doesn’t accept borrowers with credit scores of less than 600 (one of their lender safety features), so many Lending Club applicants are turned away. Upon being approved, LendingClub will offer you several different loans, with various rates, terms, and monthly payments. All of this is completed in a few minutes.

Click for LendingClub Pricing and Details.

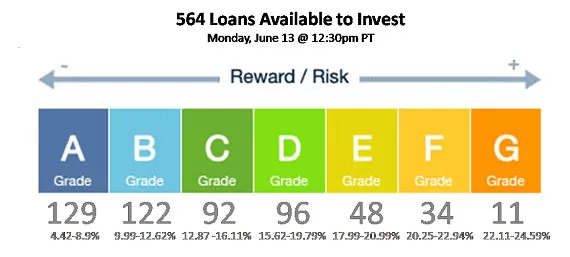

If you choose to accept one of the loan offers, LendingClub gives you a more detailed application, and assigns you a grade. LendingClub borrower grades are A, B, C, D, E, F, and G. An A grade would typically be someone with many years of good credit history, no debt, and an excellent credit score. The final interest rate offered to this person might be 5.9% – a very affordable loan! Borrowers with lower credit scores and lesser credit history will find it more expensive to borrow through LendingClub. Even so, as a debt consolidation measure, as many borrowers use it for, it’s still a good idea for many people with lower grades.

From here, your loan application is taken to a pool of investors. They won’t see any of your personal information, just the financial details of the loan request. Your loan might be funded by a single investor, or by several. Once lenders commit to fund 60% of your loan, LendingClub accelerates the remaining funding stage. Some loans won’t get to this stage of funding (1%, says LendingClub). Unfunded loan requests may be reapplied, or can be found in pieces, depending on the options Lending Club gives individual users.

Loans that get past this step are 100% funded. LendingClub verifies your bank information and may perform a hard credit check. These credit checks tell them everything they need to know about you to give them confidence in your ability to repay the loan. Hard credit checks do tend to lower credit scores, but scores go back up quickly as long as multiple hard credit checks aren’t performed in a short amount of time. Once funded, you’ll usually see the money in four business days. The whole process, from start to finish, typically takes between five days and two weeks.

Frequently Asked Questions

The LendingClub experience is pretty easy to explain at first. People lend money to other people online. But there are a lot of little details that require a little more explanations, as well as competitors who provide similar services. We’ll cover some of these popular questions from around the web, before digging deeper into this LendingClub Review.

LendingClub Vs. Prosper? Prosper and LendingClub are similar in some ways, and very different in others. Both offer simple loans with low interest rates. Both offer more affordable loans to people with excellent financial qualifications. Both take fees of about 5% when they originate your loans. Finally, both fund your loans with money from real people just like yourself.

There are important differences, however. And these differences favor LendingClub, in our estimation. We have observed that loans tend to be funded by LendingClub for lower rates than Prosper, at various lending request levels. LendingClub tends to fund their loans a bit faster than Prosper, and is available in more states (49 in fact. C’mon Iowa!).

LendingClub Vs. Sofi? Sofi and LendingClub appeal to different kinds of customers. Sofi is much more stringent in its requirements for borrowers. They don’t issue loans to anyone with a credit score lower than 700. Sofi also doesn’t charge fees for taking out loans. However, their penalties for late payments and any other nonsense are MUCH more strict. Sofi offers larger loans than LendingClub. As always, people with pristine credit will have more options than people without. Sofi may be one of those options. For people with average to good credit, LendingClub may be the better (or only) option.

What is LendingClub? LendingClub is the biggest American Peer to Peer lending company, where real people lend money to other real people at mutually beneficial rates.

What is the minimum credit score for LendingClub? 600 is the lowest score that LendingClub will accept. Those with lower scores need not apply.

Can I have two loans from LendingClub? Yes, but you’ll have to complete 12 consecutive monthly payments before you’ll be able to apply for a second loan. In some cases, LendingClub may offer second loans to qualified buyers, but it’ll be one successful year of repayment before borrowers can apply on their own.

Can I trust LendingClub? You can. LendingClub is registered with the SEC. Despite the sudden resignation of their CEO earlier this year, LendingClub’s fundamentals are solid. The loan you sign up for is guaranteed, and the terms will not change. Only you can decide if a given loan is financially right for you, but the loan itself is set in stone.

Is LendingClub a Legitimate Business? It is. LendingClub provides a necessary service within the American lending market. Their loans are often more accessible to borrowers than bank loans, and can usually be issued much faster. Savings, speed, and access are great, but LendingClub is also a fully compliant American lender with the Stock Exchange Commission.

How to invest in LendingClub. Potential lenders sign up on the LendingClub website, just like borrowers. They typically enjoy returns of 5%-9% annually, and can bid on all kinds of loans. Investors can choose to put money into one loan or many.

How Long Does LendingClub take? LendingClub loans are typically supplied in five to fourteen days, though exceptions and loan denials also happen.

How Does LendingClub make money? LendingClub charges origination fees of 1%-6% for each loan deal they broker. Other fees for late and missed payments apply on a case by case basis. LendingClub also charges management and service fees to their investors.

Why is LendingClub now in my state? People can borrow money through LendingClub is every US state except Iowa. 42 American states currently allow investment through LendingClub. Because P2P lending is a still a new financial model for America, it makes since that state legislators take time before allowing it.

Digging Deeper into the LendingClub Review

By now, you should understand how LendingClub works for borrowers in a general kind of way. We’re going to go into a bit more detail now, so you can understand if LendingClub is for you.

Recommended Stock Investing Posts:

- Top 10 Ways to Quickly Improve Your Trading Skills

- Roth IRA Conversion Ladder for Early Retirees: Decoded

- Why Leveraged ETFs are Better Than Futures and Options

- 3 Reasons Day Traders Need To Use Volume Weighted Average Price

- How to Supplement Your Income with Stocks

- Pros and Cons To Investing In The Stock Market Today

- The Neatest Little Guide to Stock Market Investing Book Review

- Critical Reasons To Invest In Small Cap Stocks

How Much Does LendingClub Cost?

LendingClub’s process for assigning fees is very complex. We’ll refer you to their LendingClub Rates page, which has a complete breakdown of charges for different borrower grades. Because no one knows the exact credit score and credit history factors that determine these borrower grades, it’s helpful to look at some specific examples and to read user reviews (plenty of those coming up). Here are two cost examples taken straight from LendingClub’s site:

“For example, if you receive a $6,000 36-month loan at an interest rate of 6.97% with a 3.5% origination fee of $210.00, you’ll receive a loan amount of $5,790.00 and will make 36 monthly payments of approximately $185.18 at a 9.39% APR.

In the case of a $20,000 60-month loan at an interest rate of 7.39% with a 5% origination fee of $1,000.00, you’ll receive a loan amount of $19,000.00 and will make 60 monthly payments of approximately $399.71 at a 9.57% APR.”

Another way to look at potential costs is using the average payments made by all LendingClub users. At the end of 2015, the average user had a credit score of 699, 16.2 years of credit history, income of $74, 414, and a debt-to-income ratio of 17.9% (not taking mortgages into account).

As you can see, costs depend on many different factors. If you want a loan, the only way you can know exactly how much it will cost is to apply.

LendingClub for Investors

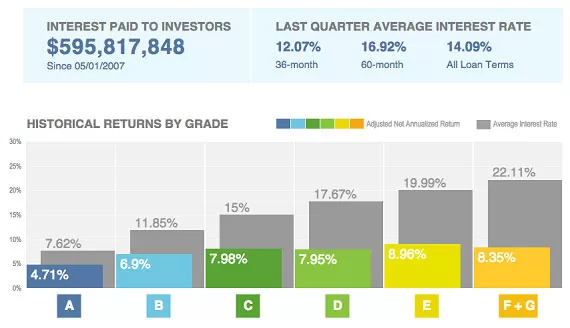

LendingClub investment is not the focus of this review, but we’ll take a little time to cover it. LendingClub advertises 5%-9% returns for investors, with 3%-6% monthly cashflow, and <1% volatility. Anecdotal reports seem to indicate that individual results may vary. Some users report returns of well over 10% annually, while others don’t seem to be able to master the system.

Because investors get to select the loans they finance, and the more money invested the more diversification can be achieved, it stands to reason that individual experiences will be diverse. Nonetheless, lots of investors have reported strong returns for years. Due to recent turmoil (details below) at LendingClub corporate, many investors have dipped out of this platform. But with the instatement of a new CEO, investors are returning. Those who return now have more loans to choose from than are commonly available.

LendingClub Controversy

At the time of this writing, LendingClub has recently overcome some internal difficulties. Audits uncovered problems related to all loans held by a single investor – to the tune of $22 million. Laplanche was found to have undeclared loan holdings. Other executives were implicated. The board acted fast, three high ranking managers were immediately sacked, and Laplanche resigned.

Since then the company has been operating as well (better?) than ever. The dust has settled and, from an outsider’s perspective, it looks like the company found an isolated problem and dealt with it. The instatement of new CEO Scott Sanborn has seen shares rise and investors return in droves. Our analysis of LendingClub’s core business model leads us to believe that the company is still solid for borrowers and investors.

In the end, what’s good for LendingClub is good for the American economy. The American borrowing market needs options for all kinds of consumers, so we’re happy to see LendingClub pull through this recent crisis and continue offering quality loans.

LendingClub User Reviews

- JonSigMan had this to say at CreditKarma:

“The system that LendingClub uses is simple to use, easy to understand, and efficient. The application process was smooth and painless. The options that were available were the only thing that slowed down the process, I had to choose which one worked for me, as they presented many potential options. It was also interesting to watch the funding process, which only took a few days, and once that was complete, funding was quick and easy. I am impressed, if you are looking for a personal loan, this is a great place to start looking.”

- Jerome had this to say at WealthPilgrim:

“I have almost $8,000 on a high interest credit card and a credit score of 663. After reading some negative reviews I was reluctant to try LendingClub. But I decided to give them a chance anyway. Afterall, I had nothing to lose by applying. But I have to say it was the easiest experience I’ve ever had in getting a loan. The online application took only a few minutes and I didn’t have to send them any supporting documentation. I was approved for a loan within 24 hours and the money was in my account within 4 business days after my initial application. The interest rate was far lower than the interest rate on my credit card. I will be debt free in only 36 months or less! I am definitely happy with my decision to try LendingClub.”

- Monica M had this to say at WealthPilgrim:

“After checking YouTube and other sources we decided to give it a try. What did we have to lose. It was the most easiest process I have ever done. Within 30 hours we were fully funded. By the next business day, the money was in our account. Thanks to those of you who wrote a good review. If it hadn’t been for those, we may not have got all our high interest loans paid off. We are saving about $300 a month in monthly payments. Thanks to all the investors who helped us get fully funded. We won’t let you down.”

- Brandy at LendingMemo had this to say: “It worked for us…it took 7 business days from start to finish. We qualified for $12,200 but only applied for $1,200 to start with to make sure it was legit and everything worked out. We also needed 17,000 to consolidate all our debt so we didn’t want to do it unless we got full amount. Anyway, our rate was 14% (low for us b/c rates otherwise from different sources range from 19-27%) with a score of 665. We will pay this off quickly and apply for the full amount we needed.”

- TXCatholic had this to say at ReadyforZero:

“I was skeptical but had a great experience. Credit score isn’t perfect but was funded $11.5k for debt consolidation. Application process was simple and money deposited into my bank account within a week of application. Interest rate is 10.9 apr and I was able to pay off those crazy high interest credit cards. There was an origination fee tacked on to the base loan amount but that was disclosed up front. I am quite pleased.”

Conclusion

LendingClub is a remarkable platform for borrowers and investors. While investing with LendingClub takes some learning and effort to achieve the best results, the borrower experience is very easy to understand and enact. While some people are disappointed that their credit score or history disqualifies them for a LendingClub loan, qualified borrowers find the platform to be very efficient. All payment terms are communicated clearly, before any commitments are made, and the loan itself is often very affordable.

Recent upheaval at LendingClub corporate has some worried about the company. But with a new CEO and solid fundamentals, we believe that the borrower’s experience of Lending Club shouldn’t be any different than before. That leaves potential users with the final question: Is LendingClub for me? Only you can ultimately answer that question…but here’s how Good Credit Info makes these considerations.

LendingClub is a very strong lender option for customers with one or more of these characteristics (the more you have, the better LendingClub may be for you):

- Need a loan fast

- Have been denied a loan from a traditional lender

- Have good to great credit

- Love the idea of borrowing from an easy, online platform

- Need to consolidate credit card or other high-interest debt

- Need to infuse a business with cash

- Need a loan for any life improvement goal, but don’t have the support of an American bank, for whatever reason

If you can relate to any of the above, LendingClub may offer real value to you. LendingClub is just one of several loan options available to people today. What’s more, the stronger your credit score and credit history, the more options will be available to you. But no one should overlook LendingClub, simply because P2P lending is unfamiliar. It’s a great option that takes enormous financial institutions out of the equation. In most cases, it’s ultimately much better for borrower and lender/investor. Get the money you need while taking part in the next generation of American lending, with LendingClub.

Disclaimer:

All loans made by WebBank, Member FDIC. Your actual rate depends upon credit score, loan amount, loan term, and credit usage and history. The APR ranges from 6.95% to 35.89%. For example, you could receive a loan of $6,000 with an interest rate of 7.99% and a 5.00% origination fee of $300 for an APR of 11.51%. In this example, you will receive $5,700 and will make 36 monthly payments of $187.99. The total amount repayable will be $6,767.64. Your APR will be determined based on your credit at time of application. *The origination fee ranges from 1% to 6%; the average origination fee is 5.2% (as of 12/5/18 YTD).* There is no down payment and there is never a prepayment penalty. Closing of your loan is contingent upon your agreement of all the required agreements and disclosures on the www.lendingclub.com website. All loans via LendingClub have a minimum repayment term of 36 months or longer.

†Per reviews collected and authenticated by Bazaarvoice in compliance with the Bazaarvoice Authentication Requirements, supported by anti-fraud technology and human analysis.

Claim: “Funding in as few as 3 days”

Disclaimer: Based on approximately 60% of borrowers who received offers through LendingClub’s marketing partners between January 1, 2018 to July 20,2018. The time it will take to fund your loan may vary.

Click for LendingClub Pricing and Details.

Rating: 4.4 / 5![]()

![]()

![]()

![]()

One other problem I have with any peer-to-peer lending is the amount of time it can take to get your money back. Loans at Lending Club are for 3 years. It will take at least that long to get your money back. It can take longer then 3 years if a borrower had trouble making payments and renegotiated their minimum payments.

Hey Bryce, the 3 year wait does suck, but most investments are long term. If you need money in 3 months, chances are, savings accounts are your best bet for making sure that’s available. Thanks for your comment!

From what I understand the investment returns are taxes as ordinary income because it’s interest income. I’m not sure if that’s 100% true in all cases, but either way, it certainly puts a dent in the returns, particularly given the risk and relative treatment of an index fund.

Hey terrible husband, thanks for your comment. This is very true. With most investments, interest earned is taxable income. However, the taxes are only a small piece of the interest earned not your total balance. So, in my book, it’s still worth investing!

I do have a small amount in lending club just for fun, but I don’t know if I’d invest a lot into it. I do think it is taxed as interest income. I think there are more investors than borrowers nowadays because there aren’t many loans that I’d like to invest in. I’m kinda conservative in the loans I invest in.

Hey Andrew, are you earning any money with your investments? I’d love to know as I’m sure some other readers would. Anyway, thanks for stopping by and sharing your thoughts!

I really like my account with Lending Club but their secondary market to sell loans isn’t very easy to work with. This isn’t an issue because I plan on holding things for the long haul. If I needed to access the money quickly, I would have some trouble getting access to the money.

Hey Micro, thanks for your comment! I don’t know much about the secondary market, but could understand how that could be a bit lacking. When it comes down to it, I never invest money I think I’ll need access to before the investment is mature. So, I don’t think that would be a problem for me. Thanks again!

Good article on Lending Club! I was ready to sign up and throw $500 or so in to see what I can make without risking too much. But apparently they don’t accept new accounts in North Carolina! Boo. Anyway, looks like a neat program to make way more than what the banks are paying on deposit accounts.

Hey Justin, thanks for your comment! I didn’t know they didn’t allow new accounts in North Carolina. Any idea of other states that might be a problem in? Thanks again!

This article really gives me a lot to think about. I’ve been looking into peer to peer lending so this was very helpful.

Hey Romona, thanks for your comment! I hope you find success in your investing adventures!

Joshua,I think you did a pretty good job describing how LC works.

I am very active in this area. You’re very right about the need to diversify loans and that interest is taxed as ordinary income. Like all fully amortizing loans (think mortgage), more of the payment goes to interest in the early months and more towards principal in the later months.

keep up the good work.

Stu

sounds like a good, open and honest lender!

For personal loan, borrowing money for buying personal stuffs is not a good idea, I would rather spend them in some investment like opening a small business or real estate, that would be a great chance to generate income to cover your loan interest.

I’ve used Lending Club for about a year now. Overall, my experience has been pretty positive. One issue.. I seem to get stuck with borrowers who are looking to pre-pay back their loan quickly. A number of my investments have been fully repaid within just a couple months.